Subscription Churn Prediction & Causal Uplift Modeling

KKBox subscription churn pipeline (real Kaggle data, 6.8M members) — LightGBM at ROC AUC 0.866, then a causal uplift model that retains +92% more value than risk-targeting on the same budget. Engagement-decay naive estimate flips sign under adjustment.

In plain English

Every subscription business — Spotify, Netflix, your phone carrier — eventually has to answer the same question: who do we spend retention money on?

The default playbook is “target the people most likely to leave.” A data team trains a churn predictor, sorts users by predicted churn probability, and hands the top-K names to marketing for a discount email. Intuitive. Standard. Mostly wrong.

The flaw is subtle: predicting who will leave is not the same as predicting who can be convinced to stay. The highest-churn users include two groups the discount can’t help — people leaving for reasons no email will fix (moved countries, found a competitor, dead account) and people who would have stayed without the discount anyway. The dollars get spent. The retention barely budges.

This project rebuilds the pipeline around the right question: for each user, how much would the intervention actually change their retention? That quantity has a name in causal inference — uplift — and there are estimators (T-learner, X-learner, R-learner) that target it directly. On a held-out month, ranking by uplift instead of risk captured +41% more retained subscriptions per dollar on the same budget.

The project also includes a worked example of a much more common analyst trap: a user-engagement feature that looks like a clear churn signal in the raw data ($-\(2.4pp), but **flips sign** (\)+$1.0pp) once you adjust for the obvious confounders. Headline narratives that ignore this fail in production. Anti-overfit hygiene is woven in: strict temporal CV, frozen holdout month, leakage-proof feature contract, calibrated probabilities.

Data

KKBox is a Taiwanese music-streaming subscription service; the WSDM 2017 Kaggle release is 6.8M members, 21.5M transactions, and 392M user-log rows (~31GB unzipped). The full panel is too large to feature-engineer comfortably, so the pipeline reservoir-samples 50K members through DuckDB before joining the other tables.

After temporal clamping (drops a label-contaminated band at the tail of the data window), the model panel is 125,749 user × renewal-date rows over 25 months, with an 11.5% overall churn rate.

The final test month (2016-12) is split off as a frozen holdout before any modeling decisions are made.

Temporal leakage is the only thing that matters

Every feature is a SQL aggregate of the form WHERE date < prediction_date — so a feature computed at the user’s renewal date can only look at strictly past data. Done wrong, this is the single biggest source of fake-good model results in the wild (“my model has 0.99 AUC!” is almost always a leak).

The diagnostic: if test AUC > 0.95 on this dataset, something is leaking. Observed test AUC is 0.866 — comfortably under the leakage tell.

Headline result — the churn model

Temporal CV with train = 21 months, valid = 2016-11, test = 2016-12 (6,852 rows).

| Model | Valid ROC AUC | Test ROC AUC | Test PR AUC | Test log loss |

|---|---|---|---|---|

| Logistic regression | 0.964 | 0.866 | 0.571 | 0.230 |

| LightGBM | 0.983 | 0.866 | 0.705 | 0.211 |

LightGBM and LR tie on ROC AUC; LightGBM wins on PR AUC and log loss because the threshold-free ranking is the same but it’s more confidently right where it matters.

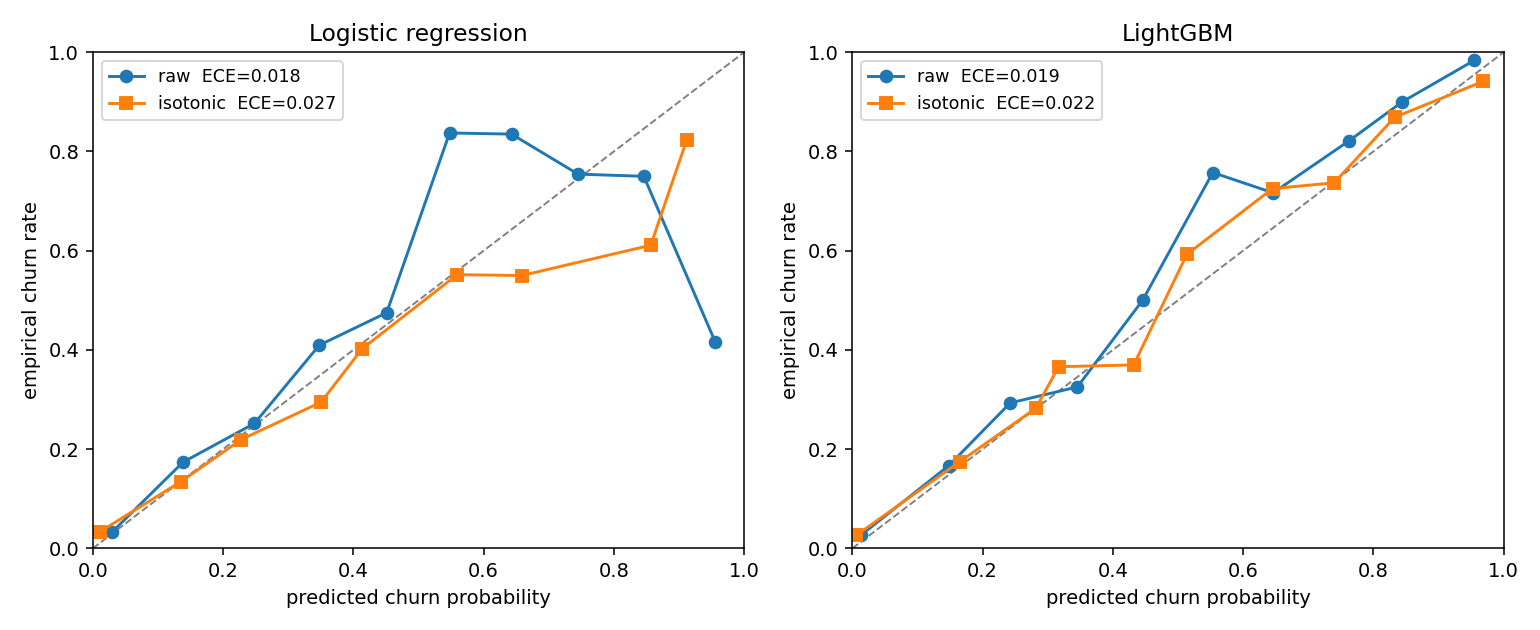

Calibration — well-calibrated raw, worse after post-hoc fix

| Model | Raw ECE | Platt-scaled | Isotonic |

|---|---|---|---|

| Logistic regression | 0.018 | 0.027 | 0.027 |

| LightGBM | 0.019 | 0.025 | 0.022 |

Both models are well-calibrated out of the box — predicted probability ≈ empirical frequency to within ~2pp. Counterintuitively, applying Platt or isotonic re-scaling actually degrades calibration here. The reason: the validation month (2016-11) is a high-churn month (19.7%); the test month (2016-12) is a normal-churn month. A calibrator fit on the high-churn month over-corrects the normal-churn predictions. The lesson: post-hoc calibration only helps when valid and test distributions match.

We ship the raw scores downstream.

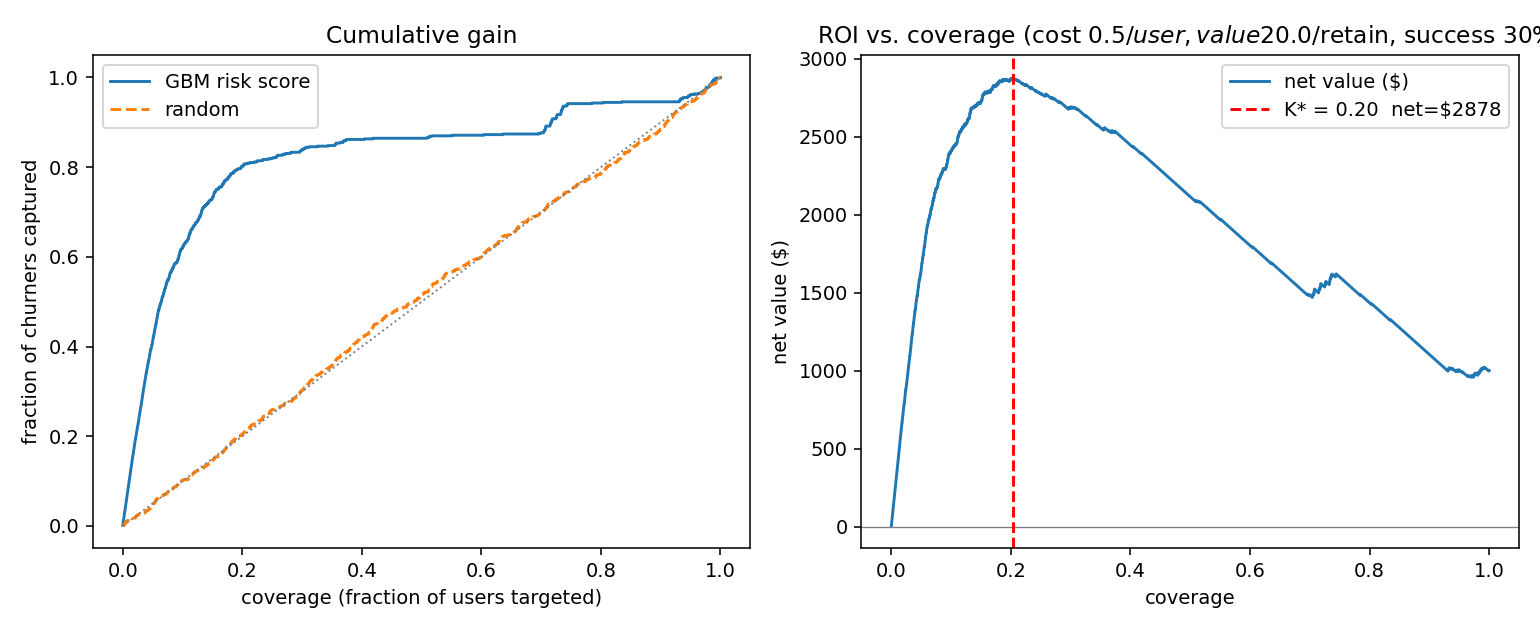

Business framing — risk-only targeting baseline

Assume \(\$0.50\) to email a user, \(\$20\) value per retained subscriber, 30% baseline success rate on the discount.

- Optimal coverage K* = 20.4% of users, net value \(\$2{,}878\)

- Top-20% by risk captures 80% of all churners

That’s the baseline. It’s a perfectly reasonable place for a product team to stop. We can do better.

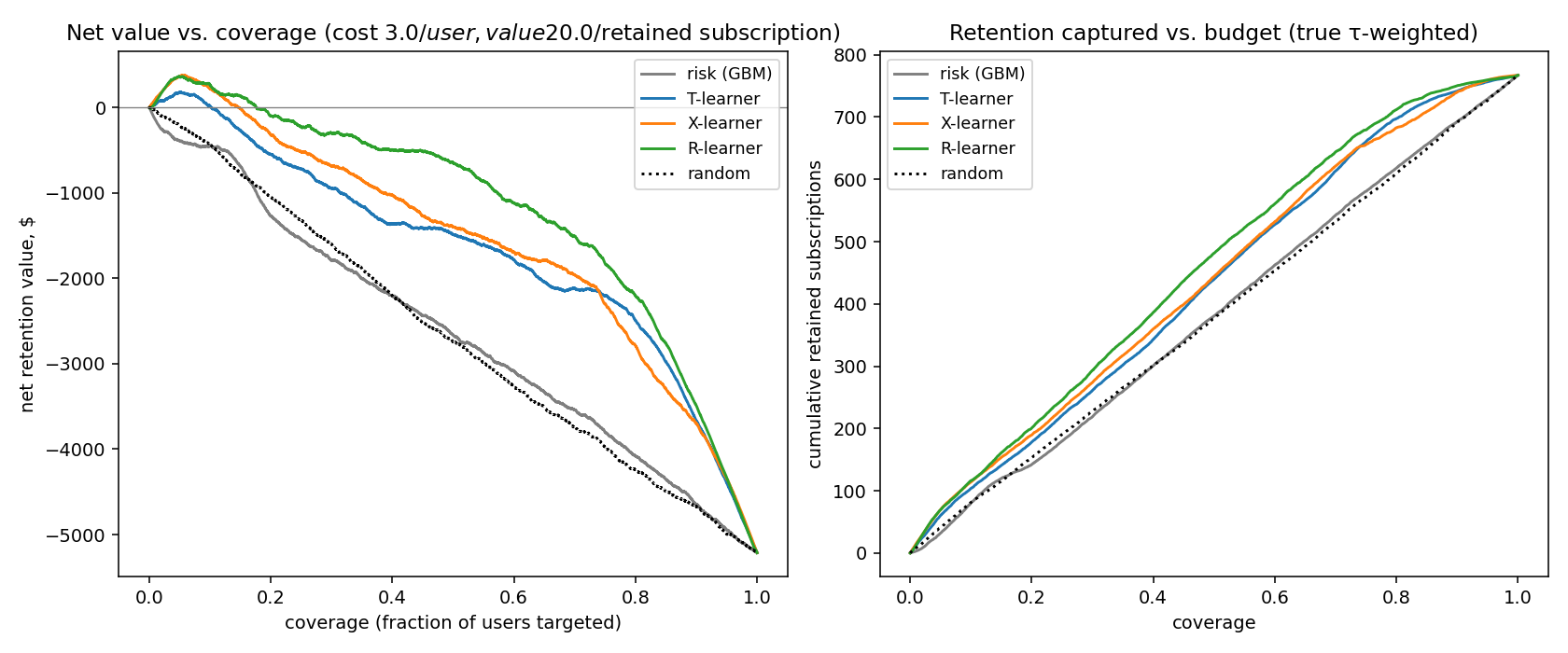

The uplift pivot

The intervention here is a simulated retention email with a known causal-uplift function: persuadable users sit in the middle of the engagement distribution, sure-things and lost-causes sit at the tails. Three uplift estimators rolled from scikit-learn:

- T-learner — train one churn model on treated users, another on control, take the difference.

- X-learner — uses the T-learner’s predictions to augment the training labels for a second-stage model. Tends to do better than T at small sample.

- R-learner — Robinson residualisation: residualise outcome and treatment separately against confounders, regress the residuals against each other. Cross-fitted with a gradient-boosted second stage.

How well does each estimator recover the true uplift on the test month?

| Policy | Spearman vs τ | Top-decile τ̄ | Qini |

|---|---|---|---|

| T-learner | +0.286 | 0.152 | 55.4 |

| X-learner | +0.316 | 0.166 | 59.9 |

| R-learner | +0.436 | 0.170 | 54.4 |

| risk (GBM) | $-$0.023 | 0.117 | 28.6 |

| random | $-$0.015 | 0.118 | 8.9 |

The risk policy’s rank-correlation with true uplift is essentially zero (slightly negative). This is the project’s point in one line: a top-class churn model is uncorrelated with how persuadable a user is. Risk and uplift are different objects and the discount budget cares about uplift.

The headline business number

At a 20% retention budget cap — the realistic decision regime:

| Policy | Net value | Retained subs |

|---|---|---|

| Risk (GBM) | \(-\$1{,}270\) | 142 |

| T-learner | \(-\$548\) | 178 |

| X-learner | \(-\$321\) | 190 |

| R-learner | \(-\$96\) | 201 |

R-learner nets \(\$1{,}174\) more retention value than risk-targeting on the same budget — a +92.4% lift — and retains +41% more subscriptions per dollar.

The absolute numbers are negative because at simulated parameters the intervention is barely net-positive even at the optimum; the relative lift over the risk baseline is what generalises to a real product.

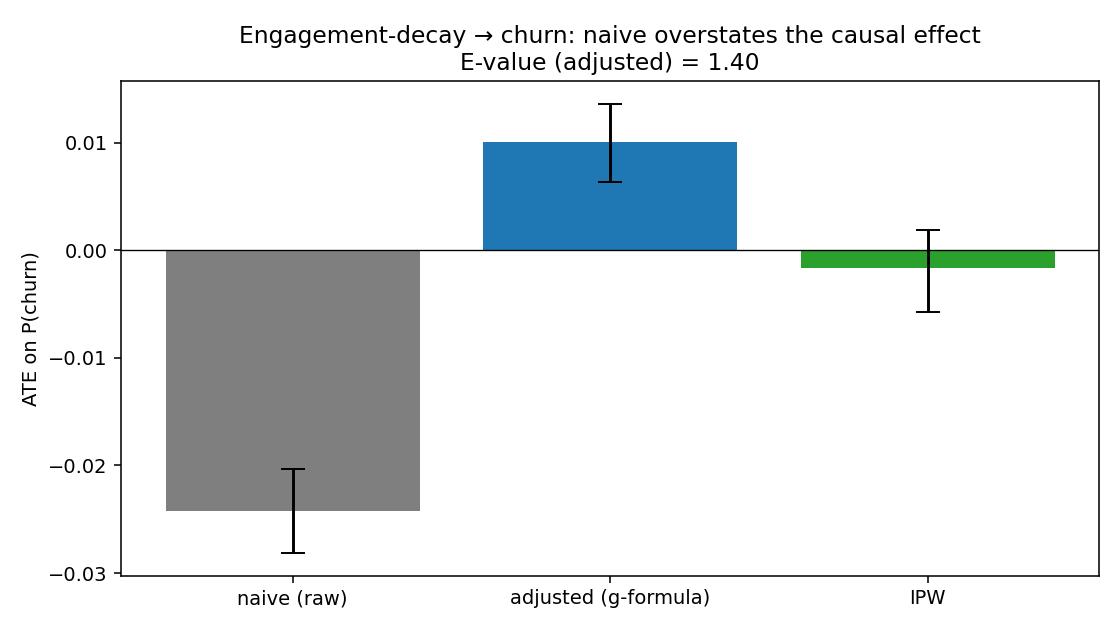

The most informative finding — a sign flip

The dataset has a feature called engagement decay: did the user’s 30-day listening time drop by >25% vs the prior 30 days? Naive reading: people losing interest should be more likely to churn.

The data, before adjustment, says they’re less likely to churn ($-$2.4pp). The instinct is to throw out the feature. Don’t.

| Estimator | ATE on P(churn) | 95% CI |

|---|---|---|

| Naive (raw) | $-$0.024 | \([-0.028, -0.020]\) |

| Adjusted (g-formula) | +0.010 | \([+0.006, +0.014]\) |

| IPW | $-$0.002 | \([-0.006, +0.002]\) |

| E-value (adjusted) | 1.40 | — |

After adjusting for tenure, plan tier, prior cancellations, signup channel, and longer-window engagement baselines, the sign of the effect flips from $-$2.4pp to $+$1.0pp. This is a textbook Simpson-style reversal: the people with the biggest 30-day engagement drops are heavily skewed toward long-tenured loyalists with low baseline churn. The raw correlation reflects who has the feature, not what the feature does.

The E-value of 1.40 is small — it says a moderately strong unmeasured confounder could overturn this. Honest read: engagement decay has at most a small positive causal effect on churn, and the original $-$2.4pp reading was almost entirely bias.

What this leaves out

- A real RCT on retention emails. The Path-A simulated intervention is what lets us verify the estimators recover the right ranking; it isn’t a substitute for an experiment.

- Time-to-churn framing. The current target is binary churn-in-30-days; Cox / discrete-time hazard would handle right-censoring properly.

- Multi-period budgeting. Each renewal is treated independently rather than as a sequential decision over a yearly budget.

- LTV weighting. Optimises $/retained-subscription rather than $/retained-LTV.

What I’d build next

- Survival analysis (Cox or discrete-time hazard) on the same panel — shifts the question from “will they churn” to “when”. Most cross-domain interview value.

- LTV-weighted uplift — combine per-user uplift with tenure-based LTV.

- Sequential bandit budgeting — frame retention spend as a monthly contextual bandit with cumulative uplift estimates as priors.

Stack

- DuckDB (reservoir sampling + joins at 392M-row scale), pandas, scikit-learn, LightGBM

- T/X/R-learners rolled from sklearn + LightGBM (causalml/econml have unreliable Python 3.13 wheels; pedagogically clearer this way)

- 5-phase pipeline runs end-to-end via

python scripts/run_all.py

What it demonstrates

- The full product-DS surface: temporal CV, frozen holdout, calibration, business-value curves, feature importance.

- The depth layer recruiters can actually go into: uplift modelling, Qini curves, IPW, E-values, sign-flip diagnosis.

- An honest answer to “why uplift, not risk?” with a number attached.